UK Crackdown on P2P Crypto: A Regulatory Pivot | ChainPulse

Regulation

UK Crackdown on P2P Crypto: A Regulatory Pivot

UK FCA raids 8 London addresses for unregistered P2P crypto trading. The message: crypto businesses must register under AML rules or face criminal probes.

The FCA is not banning P2P; it's demanding that every crypto business play by the same AML rules as traditional finance.

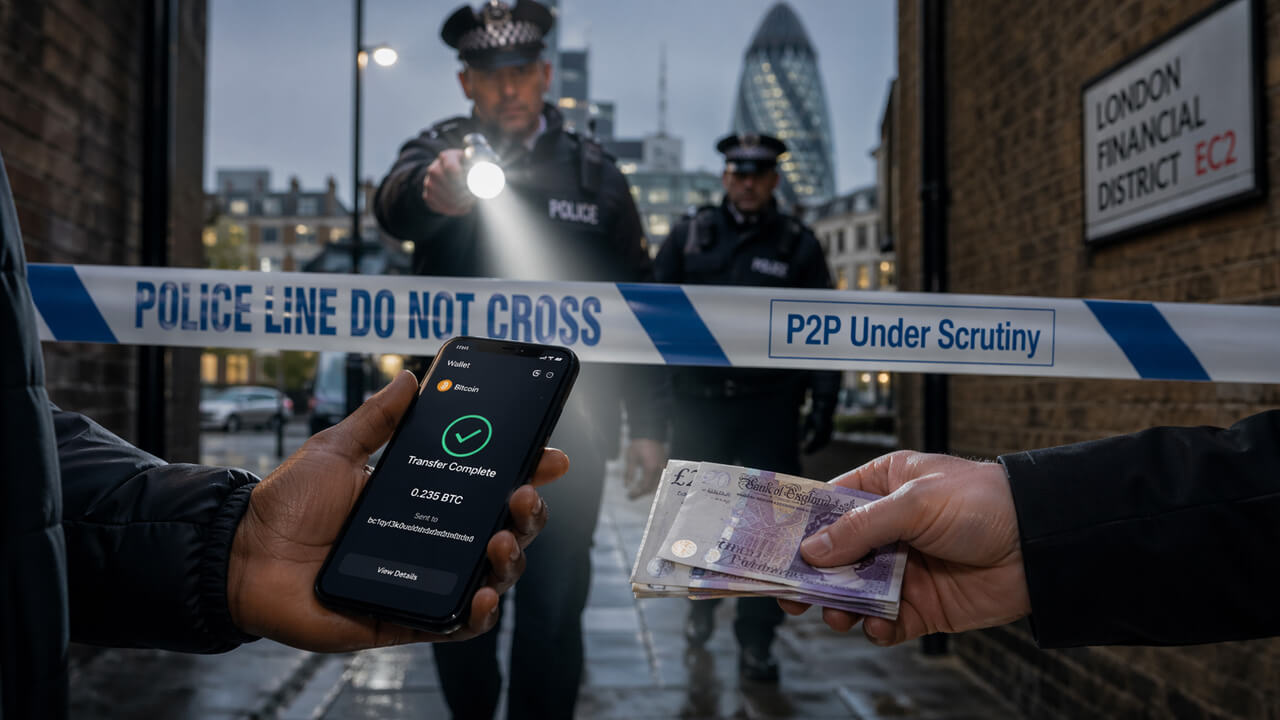

Police knocked on eight London doors this week, but they weren't looking for drugs. They were looking for unregistered crypto traders. The U...

The FCA coordinated with police and tax authorities to visit eight London addresses linked to suspected illegal peer-to-peer crypto trading....

Police knocked on eight London doors this week, but they weren't looking for drugs. They were looking for unregistered crypto traders. The UK's Financial Conduct Authority (FCA) just sent its clearest signal yet: peer-to-peer crypto dealing is a regulated business, and operating without a license is a crime.

The Signal

The FCA coordinated with police and tax authorities to visit eight London addresses linked to suspected illegal peer-to-peer crypto trading. At each location, officers issued cease-and-desist letters and gathered evidence that now supports criminal investigations. According to Reuters, there are zero FCA-registered peer-to-peer crypto traders in the UK. That means every person who regularly buys and sells crypto for others, advertises their service, or handles customer money is operating outside the law.

police raid on London address

The legal line is straightforward. Occasional person-to-person trades don't trigger registration requirements. But the moment someone turns it into a business—repeated exchanges, advertising, handling client funds—they become a "cryptoasset exchange provider" under the UK's Money Laundering Regulations. Registration with the FCA is mandatory before starting operations. The regulator's anti-money laundering regime explicitly includes P2P providers.

“The FCA is not banning P2P; it's demanding that every crypto business play by the same AML rules as traditional finance.”

On-Chain Data

On-Chain Data

Registered P2P traders: Zero. No P2P crypto trader is registered with the FCA, per Reuters.

Addresses visited: 8 London locations in coordinated operation.

Action taken: Cease-and-desist letters plus evidence collection for criminal probes.

Legal scope: UK AML rules cover "cryptoasset exchange providers," including P2P, since 2020.

on-chain analytics dashboard

Market Impact

This operation marks a turning point for the UK's P2P market. Until now, many informal operators assumed person-to-person trading flew under the regulatory radar. The FCA just proved otherwise. Anyone acting as a business must register, verify customers, monitor transactions, and report suspicious activity. Failure to comply can lead to criminal prosecution.

The move also echoes the FCA's 2023 crackdown on unregistered crypto ATMs, which it declared illegal. Now the net widens to any fiat-to-crypto gateway. Centralized exchanges that are already registered in the UK benefit from this enforcement, as informal competitors are either shut down or forced to formalize.

Your Alpha

Your Alpha

For traders and investors, this crackdown carries two clear implications. First, using unregistered P2P services in the UK now carries legal risk for both operators and users who may become part of an investigation. Second, regulatory pressure on P2P could reduce liquidity in certain trading pairs and push volume toward registered exchanges or decentralized platforms.

1If you trade P2P in the UK, verify your counterparty is FCA-registered. Otherwise, you may be participating in an illegal activity.

2Consider moving volume to registered centralized exchanges (e.g., Coinbase, Kraken) to avoid regulatory and tax complications.

3For builders, this opens an opportunity: create compliant P2P platforms with built-in identity verification and transaction monitoring.

trader analyzing charts

Next Catalyst

The UK government has already announced a full cryptoasset regime under FSMA-style rules by October 2027. This will include regulation for stablecoins, custodians, and likely tighter P2P requirements. The FCA operation is a preview of what's coming: a crypto market fully integrated into the traditional financial perimeter.

Additionally, the involvement of tax authorities (HMRC) signals that undeclared income from P2P trading is also in the crosshairs. Operators who have been earning fees or spreads without paying taxes could face not just unregistered business charges but also tax evasion penalties.

The Bottom Line

The Bottom Line

The FCA has fired a warning shot across the P2P market: unregistered crypto dealing is now a criminal enforcement priority. For investors, the safest path runs through regulated platforms. For informal operators, the choice is to register or exit. The UK is building a regulatory wall that, by 2027, will be complete.

Position yourself accordingly: move to compliant platforms now, before the next wave of enforcement.

DeFi Implications

The FCA's offensive also has implications for the DeFi ecosystem. While decentralized platforms lack a central entity to register, the fiat on/off ramps are subject to regulation. P2P operators using stablecoins or wrapped tokens to facilitate trades could be caught in the regulatory net if they act as regular intermediaries. The FCA has already indicated that DeFi protocols with centralized governance could be considered regulated businesses.

On the other hand, pressure on P2P could accelerate adoption of privacy solutions like non-custodial wallets and decentralized exchanges (DEXs) that don't require KYC. However, regulators are already eyeing these alternatives. The UK has proposed rules for DEXs that would allow identity verification at the protocol level, potentially changing the landscape.

Historical Context: UK's Regulatory Evolution

Historical Context: UK's Regulatory Evolution

The UK has been a pioneer in crypto regulation. Since 2020, when MLRs were extended to crypto exchange providers, the FCA has been building an increasingly strict framework. In 2021, the FCA warned that most registration applications from crypto firms were rejected due to poor AML controls. In 2023, it declared unregistered crypto ATMs illegal. Now, the focus is on P2P.

This week's operation is not an isolated event. It's part of a broader strategy to integrate cryptoassets into the traditional financial perimeter before the full regime in 2027. The FCA has increased its crypto compliance staff and established a dedicated team to monitor unregistered activities. The home visits are just the beginning.

International Perspective: Comparison with Other Jurisdictions

The UK's approach contrasts with other jurisdictions. In the US, P2P regulation is fragmented: FinCEN requires registration as an MSB, but enforcement is inconsistent. In the EU, the MiCA regulation, which will fully apply in 2025, also covers crypto service providers, including P2P, but with a longer transition period. Singapore and Hong Kong have strict regimes but with exemptions for occasional trading.

The UK stands out for its aggressive enforcement: not only does it require registration, but it conducts raids and collects evidence for criminal proceedings. This sends a much stronger deterrent signal than administrative fines. Other countries may follow suit.

On-Chain Data: P2P Volume in the UK

On-Chain Data: P2P Volume in the UK

While exact data is unavailable, P2P trading volume in the UK is estimated in the hundreds of millions of pounds annually, based on data from platforms like LocalBitcoins and Paxful (now closed). Most transactions are in Bitcoin and Ethereum, but there is also activity in stablecoins like USDT and USDC. The FCA's offensive could shift this volume to registered exchanges or the gray market, potentially increasing the P2P premium.

Estimated volume: Over £500 million annually in P2P transactions in the UK (industry sources).

Top cryptos: Bitcoin (60%), Ethereum (20%), stablecoins (15%), others (5%).

P2P premium: Historically between 2% and 5% over market price, but could rise after the crackdown.

UK P2P volume chart

Tax Implications

The involvement of HMRC in the operation is key. P2P operators who have been earning undeclared income could face audits and penalties. HMRC has intensified its efforts to track crypto transactions using blockchain analysis and exchange data. The agency has already sent letters to thousands of taxpayers urging them to declare unreported gains.

For users, buying crypto via P2P can create problems if the seller doesn't declare. Authorities could investigate buyers as part of their probes. It's advisable to keep detailed records of all P2P transactions, including counterparty identity and fund origin.

Final Conclusion

Final Conclusion

The FCA has fired a warning shot across the P2P market: unregistered crypto dealing is now a criminal enforcement priority. For investors, the safest path runs through regulated platforms. For informal operators, the choice is to register or exit. The UK is building a regulatory wall that, by 2027, will be complete. The question is not whether more operations will come, but when and where the next one will land.